Will People Stop Saying a Recession is Coming?

The trendy online narrative has little substance to back it up

It’s in every economic TikTok video now, and some that aren’t even related to economics. “A recession is coming,” people announce, as if it’s as certain as the arrival of a Japanese bullet train. (In fact, the prediction of recessions is about as scientific as astrology and possibly less accurate.) The even cooler kids say “we’re already in a recession”—as if the telltale signs of a recession wouldn’t have been documented by anyone else. This narrative clearly originated online, but has now spread into more serious discourse, with people repeating it like it’s fact here on Substack, on other social networks, and in person.

But what evidence is there for a recession? Actually, precisely none. Let’s break it down below.

Real Recession Indicators

The commonly used definition of a recession is two consecutive quarters of negative GDP growth (although the National Bureau of Economic Research, which is responsible for announcing recessions, takes into account many more factors, and did not announce a recession the last time GDP contracted two quarters in a row). So let’s take a look at GDP: the most recent reading was a 2.4% growth and the one before that was a 3.1% growth.

It’s also key to look at the labor market. Widespread job losses affect regular Americans the most during recessions, and it’s questionable to call any period a recession that doesn’t include them. Since the end of WWII, every recession has come with an increase in unemployment, peaking at a minimum of 6%. Job creation remains similar to the numbers in the five years preceding COVID, hourly earnings continue to rise, unemployment is only 4%, and there are still almost eight million open jobs in the US, compared to, say, five million in 2015. For a labor market recession to occur, millions of those jobs would have to be filled, and many others lost.

Another reliable indicator of economic growth is the Purchasing Managers’ Index, or PMI. This gauge surveys purchasing managers regarding business orders and whether those orders are growing or falling. The median value is 50, with values over 50 denoting an expansion and under 50 denoting a contraction. In March, the PMI spiked to over 65, the highest in almost four years. By contrast, in 2023 and 2024, when no one was saying a recession was coming, they spent considerable time in contraction territory under 50.

Additionally, for there to be a recession, consumers have to stop spending money. While many wise forecasters have predicted that the consumer will finally tap out, this so far has not transpired, probably because Americans love spending money regardless of whether it’s earned, inherited, borrowed, or stolen. Retail sales, seasonally adjusted, are up for their second month in a row.

Dubious Recession Indicators

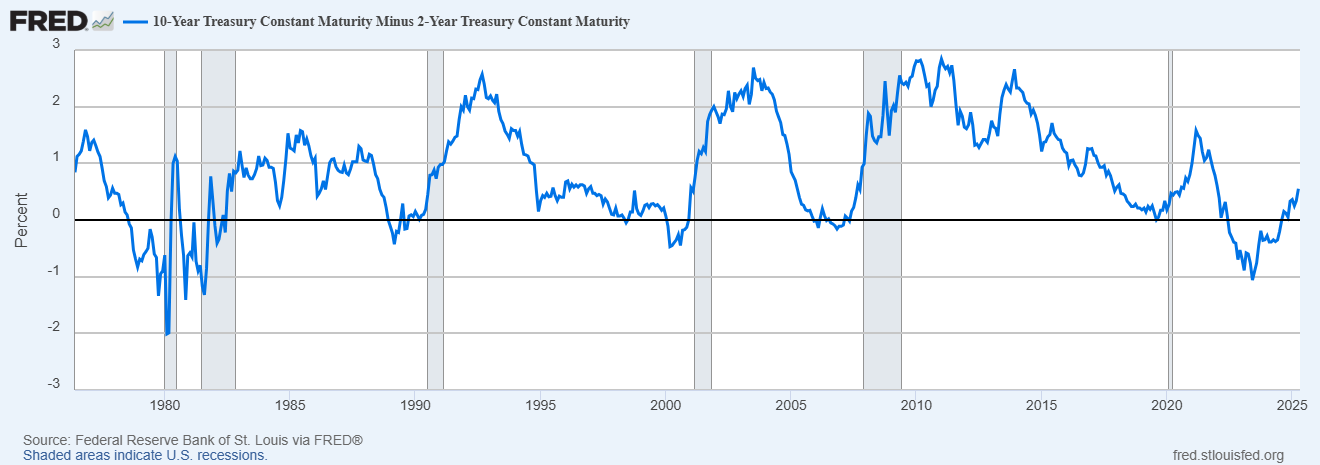

An indicator that’s talked about frequently by folks with financial knowledge is the yield curve. Subtracting the two-year note’s yield from the ten-year note’s yield gives the yield curve. For decades, an “inversion” in the yield curve (curve under zero) was considered a reliable signal of oncoming recession. This makes sense, because short-term bonds having a higher yield than long-term bonds means that investors are piled into long-term bonds, thinking that the short term is not a good place to invest.

The inverted yield curve indicator accurately predicted recessions in the early 1980s, the early 1990s, the dot-com bubble, and 2008, as well as the COVID crash (although it’s not clear how the last one wasn’t just a coincidence). However, there are a few strikes against using the yield curve as an indicator. First, it appears to be broken, seeing as it was negative from mid-2022 to mid-2024 and there was no recession. Some believe the inversion only occurred because the Fed artificially inflated short-term maturities by hiking. An additional strike against using the inverted yield curve is that it is no longer inverted, and has in fact risen sharply in recent months, so is no longer predicting a recession.

The second dubious indicator is credit spreads. These measure the difference in interest rates between high-yield bonds (“junk bonds”, if you will) and Treasuries. Like the inverted yield curve, credit spreads are sensible as a recession indicator: when times are good, investors won’t mind holding junk bonds, as bankruptcies are rare, but when push comes to shove, they will demand much higher rates than they would from an investment-grade instrument.

Unfortunately, credit spreads also have a record of false positives. While they accurately predicted the 2000 and 2008 recessions, they spiked in 1998, 2002, 2012, 2016, and 2022 without a recession materializing. While they have increased lately, spreads are still only at 3.75%, versus a long-term historical average of 5.25%.

Conclusion

With businesses, jobs, sales, and GDP all in good shape, it’s hard to see how a recession occurs. Of course, it still could, but there’s no evidence to suggest it as of yet. There’s a difference between speculation (“tariffs will cause a recession”; “the stock market crash will cause a recession”—either or both of which could potentially be true) and facts, which don’t point to any recession at all.

Don’t fall for trendy online narratives; look at the data.