America's Worsening Debt Crisis

The Moody's downgrade only makes official what everyone already knew

Moody’s decision to downgrade the US government’s credit rating deprived the government of the last AAA rating it held among the three major ratings agencies. The news caused the market to finally have a major down day, its first significant one since the rebound from the tariff-inspired correction last month. In the wake of the news, risk assets sold off, but atypically, bonds sold off also, and yields rose. I felt vindicated in calling yields a joke last month, as they somewhat adjusted to reflect reality (though, I would argue, still not as much as they should).

I’m happy the downgrade occurred because I think it has brought the US’s budget issues to front of mind. This is an emergency that everyone should know about. So in lieu of the usual stock pick or pattern analysis, I will focus on this issue in this post.

Here are a few salient points regarding the debt, courtesy of the wonderful yet terrifying US Debt Clock website:

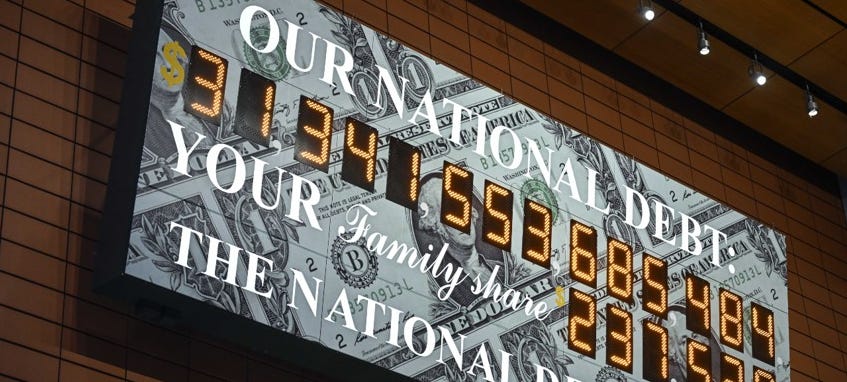

In total, the debt is nearly $37 trillion, or about $100,000 per American citizen

When you consider that children, the elderly, and the unemployed are not taxpayers, the debt per capita is significantly higher

The debt comprises 120% of GDP, up from about 35% in 1980

Interest on the debt is about 20% of federal tax revenue, and a larger annual expense than the United States’ entire defense outlay

Read that last point again. Interest on the debt is now costing the US government more than it spends on defense—to maintain by far the most powerful military in the world, with a footprint in every continent, advanced weaponry, and constant research and development to keep improving.

How did we get here?

As mentioned above, in 1980, the debt to GDP ratio was an excellent 35%. So what happened? A picture tells a thousand words.

During the long period of prosperity that started after the end of WWII, the United States had no reason to run up enormous debts, and the era of sound money with a gold standard, low inflation, and prioritization of the budget by politicians continued for decades. Even after President Nixon broke the peg to gold in 1971, the debt to GDP ratio remained tame.

But then came President Reagan, who faced a difficult bind. He wanted to do two things at once: pass a gigantic tax cut, and expand military spending so as to outspend the Soviet Union and force them into an arms race that would lead to their bankruptcy and collapse. There was no way to make up the shortfall caused by simultaneously dropping revenue and increasing spending. So Reagan let the budget go into a deficit—a controversial decision at the time, more so than people might think now.

While in retrospect, both the tax cut and the increased military spending largely achieved their goals—the 1980s and 1990s were economic boom times, and the USSR collapsed in 1991—the era of budget deficits had begun, and there was no putting the genie back in the bottle. As the situation approached crisis, the first President Bush broke his infamous “read my lips: no new taxes” promise by raising taxes.

The nation returned to frugality under President Clinton’s tenure, but the Afghanistan and Iraq Wars under the second President Bush were expensive, and the era of both monetary and fiscal stimulus that began in 2008 and redoubled in 2020 has not ended. The problem is not so much that stimulus occurred in the depth of both recessions, but that it continued even after the economy had recovered.

This chart shows that the US government has been in a deep deficit nearly every year since the 2008 recession occurred. Only two years in this chart actually saw a recession, but all of them saw a deficit—and the cumulative effect has brought us to the point where the debt can be considered an emergency.

Where do we go from here?

Policymakers probably need to do all of the following things:

Raise taxes: The top rate on the very wealthy is only 37%, while it’s 32% for income between $190,000 and $250,000 per year. As a temporary emergency measure, taxes may need to be raised on the very wealthy—or on everyone.

Cut military spending: Despite the fact that no country could credibly attack its shores conventionally, and that it has a massive nuclear deterrent, the US spends inordinate amounts of money to maintain the best military in the world. Partly this is to protect other countries. We have troops permanently stationed in South Korea, Japan, and Germany. Scaling back this footprint could go a long way towards balancing the budget.

Cut non-military spending: While I have some disagreements with DOGE’s approach, its mission is definitely important. The federal government does not have any of the limitations that private companies do (hiring freezes, reorganizations, etc.) and as such, many of its agencies are likely bloated.

Of course, President Trump’s so-called “big beautiful bill” will do none of this. He aims to extend his tax cuts from his first term, and will not address spending in any meaningful way. However, Trump is more the rule than the exception when it comes to politicians: for decades now, they have kicked the can down the road regarding the deficit and debt, refusing to make the hard decisions that future generations direly need them to. We can only hope that will change before too long.